HDFC Bank and ICICI Bank, India's two largest private sector banks, announced their Q1 FY27 financial results on July 18, 2026. Together, these banking giants account for nearly 50% of the Bank Nifty index and around 30% of the Nifty 50, making their quarterly earnings one of the most important events for Indian equity markets.

Both banks delivered healthy earnings growth, reflecting continued strength in India's banking sector despite a challenging interest rate environment.

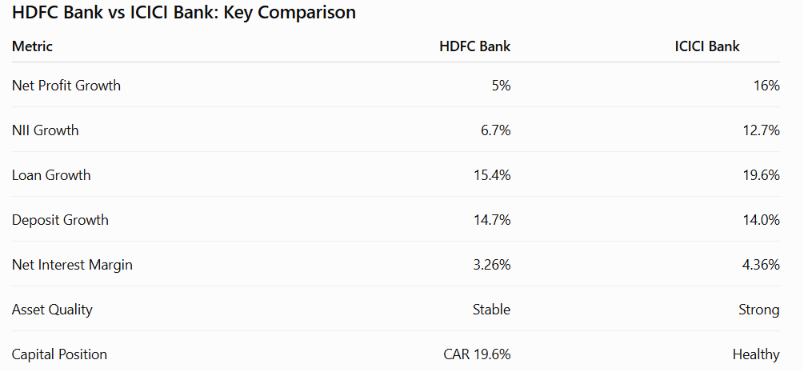

HDFC Bank reported a standalone net profit of ₹19,060 crore, registering a 5% year-on-year growth. Net Interest Income (NII) increased 6.7% to ₹33,534 crore, while gross advances grew 15.4% to ₹30.61 lakh crore. Total deposits also remained strong, rising 14.7% to ₹31.70 lakh crore.

Asset quality remained largely stable. Gross NPA stood at 1.17% compared to 1.15% in the previous quarter, while Net NPA increased slightly to 0.41% from 0.38%. The bank reported provisions of ₹3,060 crore, sharply lower than ₹14,441 crore a year ago, providing support to overall profitability. Net Interest Margin (NIM) came in at 3.26%, while the Capital Adequacy Ratio remained robust at 19.6%, highlighting the bank's strong financial position.

ICICI Bank, however, delivered an even stronger quarter. The bank reported a 16% year-on-year increase in standalone net profit to ₹14,805 crore. Net Interest Income rose 12.7% to ₹24,384 crore, supported by strong credit demand and expanding lending margins.

The bank's balance sheet continued to grow at an impressive pace. Total assets increased 14.5% to ₹24.32 lakh crore, while deposits rose 14% to ₹18.34 lakh crore. Net advances surged 19.6%, significantly outpacing HDFC Bank's loan growth. Average CASA ratio remained healthy at 38.1%, reflecting a strong low-cost deposit franchise. Net Interest Margin also improved to 4.36%, among the highest in the Indian banking industry.

Which Bank Performed Better?

Based on the Q1 FY27 numbers, ICICI Bank delivered the stronger operational performance.

The bank outperformed HDFC Bank across several key parameters, including profit growth, Net Interest Income growth, loan expansion, and Net Interest Margin. Its higher profitability and faster credit growth indicate stronger momentum during the quarter.

HDFC Bank, however, continued to demonstrate its strength through stable asset quality, robust deposit growth, significantly lower provisions, and a very strong capital adequacy ratio. While its earnings growth was comparatively modest, the bank remains one of India's strongest and most stable financial institutions.

Market Impact

Since HDFC Bank and ICICI Bank together contribute nearly half of the Bank Nifty's weight and close to one-third of the Nifty 50, their quarterly earnings are likely to have a significant influence on overall market sentiment. Strong results from both lenders reinforce confidence in the Indian banking sector and could provide support to banking stocks and benchmark indices in the near term, although investor reaction will also depend on management commentary, future loan growth guidance, and broader market conditions.

Overall, both banks delivered healthy Q1 FY27 performances. While HDFC Bank maintained its leadership through financial stability and balance sheet strength, ICICI Bank emerged as the stronger performer this quarter with superior earnings growth, higher margins, and faster credit expansion.

Disclaimer: This article is intended solely for informational and educational purposes and should not be considered financial, investment, or trading advice. The information presented is based on publicly available company disclosures and reliable sources believed to be accurate at the time of publication.