The National Statistics Office (NSO), under the Ministry of Statistics and Programme Implementation (MoSPI), released the quarterly estimates of Gross Domestic Product (GDP) for the April-June quarter (Q1) of the financial year 2025-26. The latest numbers present a positive picture for the Indian economy, highlighting strong growth momentum across sectors, especially in services, manufacturing, and construction.

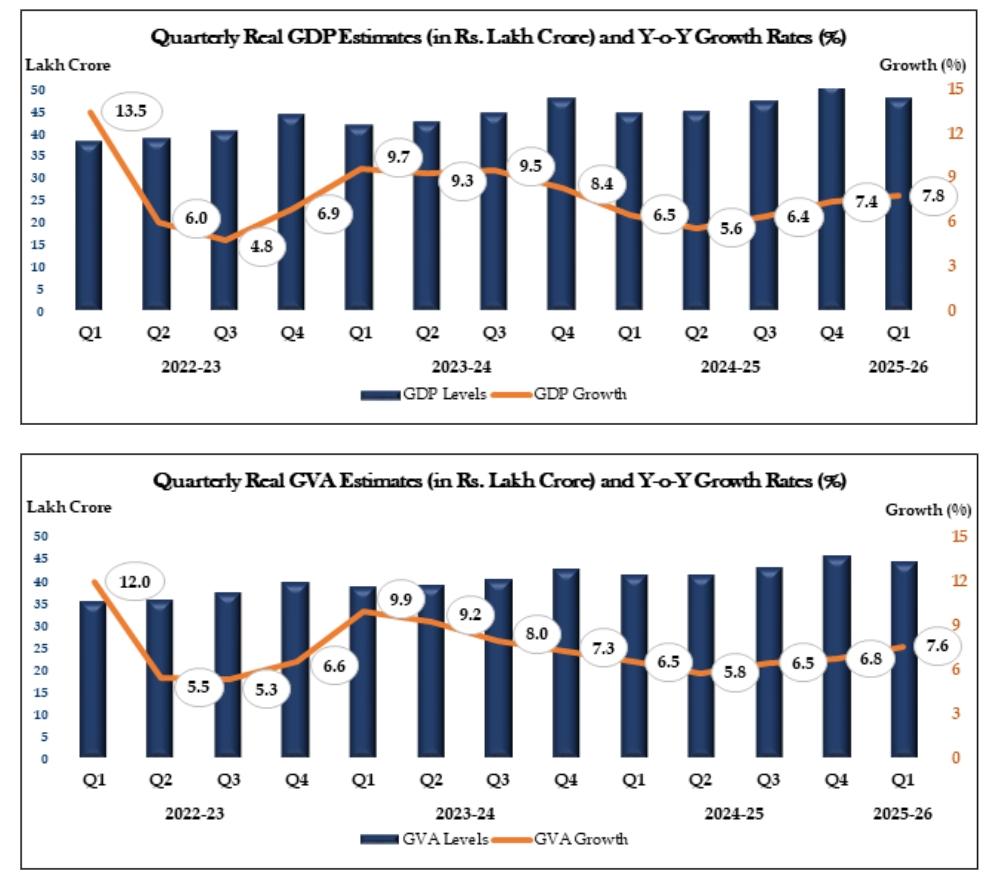

According to the report, real GDP in Q1 FY 2025-26 has been estimated to grow at 7.8%, a sharp improvement compared to 6.5% in the same quarter of the previous financial year. This performance makes India one of the fastest-growing major economies in the world, underlining the resilience of its domestic demand, investments, and robust expansion in key industries.

Nominal GDP, measured at current prices, also showed healthy growth, expanding by 8.8% in Q1 FY 2025-26. The total nominal GDP for this quarter stood at ₹86.05 lakh crore, as compared to ₹79.08 lakh crore in Q1 FY 2024-25. In real terms, GDP was estimated at ₹47.89 lakh crore, against ₹44.42 lakh crore last year.

Sector-wise Performance

One of the key highlights of the Q1 data is the buoyant performance of the services sector, which continues to drive India’s growth story. The tertiary sector posted a remarkable 9.3% growth rate at constant prices, compared to 6.8% growth in the same period last year. This surge reflects rising demand in trade, transport, communication, financial services, and other professional activities.

The agricultural and allied sector, often considered the backbone of rural demand, registered a real Gross Value Added (GVA) growth of 3.7%. This is a significant improvement from 1.5% growth seen in Q1 of the previous financial year. Better crop output, favorable weather conditions, and improved allied activities contributed to this steady expansion.

The secondary sector also displayed strength. Manufacturing grew by 7.7%, while the construction sector recorded 7.6% growth. Both these segments are crucial indicators of investment activity and employment generation, and their positive momentum highlights growing industrial confidence and demand.

However, not all sectors showed strong performance. Mining and quarrying contracted by 3.1%, reflecting sluggish demand and supply bottlenecks in natural resource industries. Similarly, electricity, gas, water supply, and other utility services grew at just 0.5%, showing a moderation compared to the robust growth recorded in earlier quarters.

Expenditure-Side Trends

On the expenditure front, government spending made a strong comeback. Government Final Consumption Expenditure (GFCE) registered a 9.7% growth rate in nominal terms during Q1 FY 2025-26, a substantial rise from 4.0% growth recorded in the same period last year. This indicates a higher level of fiscal activity and capital spending by the government, likely aimed at boosting infrastructure and welfare programs.

Private Final Consumption Expenditure (PFCE), which reflects household spending and accounts for a major share of GDP, recorded a 7.0% real growth rate. While this is slightly lower than the 8.3% growth rate seen in Q1 FY 2024-25, it still demonstrates resilient consumer demand despite global uncertainties and inflationary pressures.

Investment activity also remained robust. Gross Fixed Capital Formation (GFCF), which is a proxy for investment in infrastructure and business expansion, posted a 7.8% growth rate at constant prices. This was an improvement from 6.7% growth recorded in Q1 FY 2024-25, pointing towards higher capital spending and industrial investments.

Implications for the Economy

The Q1 GDP numbers reaffirm India’s position as the fastest-growing major economy, supported by structural reforms, resilient domestic demand, and recovery in key sectors. The strong performance of services and manufacturing is particularly significant, as these sectors are both labor-intensive and crucial for sustaining long-term economic growth.

The recovery in agriculture provides optimism for rural demand, which in turn supports consumption. At the same time, government spending and private investments are providing a dual push to growth momentum. The only weak spots are the mining and utilities sectors, which continue to face challenges due to external demand shocks and domestic supply constraints.

The outlook for the coming quarters will depend on global trade conditions, inflation trends, and monetary policy stance. While geopolitical uncertainties and global slowdown risks remain, India’s domestic fundamentals appear strong enough to maintain steady growth in the range of 7% and above for FY 2025-26.

Conclusion

India’s Q1 GDP growth of 7.8% is a clear indication that the economy has entered the new financial year on a strong footing. The broad-based expansion across agriculture, manufacturing, construction, and services reflects healthy economic fundamentals. Though certain sectors like mining and utilities lagged behind, the overall momentum is encouraging.

As private consumption, government spending, and investment activity continue to expand, the Indian economy is well positioned to retain its status as a global growth leader. The coming quarters will further test the resilience of this momentum, but for now, the Q1 data paints a picture of confidence, stability, and strong economic potential.